Interest is a fee for borrowing money. When people invest their money, the bank pays them interest because the bank has, in effect, borrowed money from the depositor. Conversely, when people take a loan or mortgage , they pay interest to the bank. In most cases, this is compound interest , which means the interest is paid not only on the amount of the original deposit, but also on any accrued interest. In contrast, simple interest is only paid on the original deposit. The effect of this is that the amount of interest earned each year does not change with simple interest, but it increases with compound interest.

Comparison chart

| Compound Interest | Simple Interest | |

|---|---|---|

| Introduction (from Wikipedia) | Compound interest arises when interest is added to the principal, so that, from that moment on, the interest that has been added also earns interest. This addition of interest to the principal is called compounding. | Simple interest is calculated only on the principal amount, or on that portion of the principal amount that remains unpaid. |

| Formula for calculation | A = P * {(1 + r)^n}, where A is the total amount due if a principal P is invested at a compound interest rate of r per period, and n is the number of such periods. | A = P * r * n, where A is the amount due when the principal P is invested at a rate r for a time period n. |

What is simple interest?

Interest is a fee for borrowing money. The greater the amount borrowed ( principal ), the greater the fee. So interest is usually calculated as a percentage of the principal. This percentage is called the interest rate . For example, if $100 was borrowed at 10% per year for 1 year, the amount to be repaid at the end of the year would be $110.

Simple interest formula

The mathematical formula for calculating simple interest is

where r is the period interest rate (the interest rate I divided by the number of periods m t ), B 0 the initial balance and m t the number of time periods elapsed.

<iframe width=”450″ height=”338″ frameborder=”0″ allowfullscreen src=”https://www.youtube.com/embed/GtaoP0skPWc?iv_load_policy=3&rel=0″></iframe>

What is compound interest?

Simple interest is rarely used in common loans and deposits because of the time value of money. When interest earned in a specific period is added back to the principal, this is called compounding . This means in the next period, interest is calculated on the new (higher) amount rather than the original amount. In effect, the principal keeps increasing as interest is accrued, resulting in ever higher interest income. Over a long period of time, this makes a huge impact on earnings. This phenomenon is called the magic of compounding and is further explained in the example below .

Compound interest formula

The mathematical to calculate compound interest is

where A is the amount or future value of the deposit, P is the initial deposit amount (or present value), i is the effective interest rate per period, and n is the number of periods.

Note that since this is an exponential function, the amount increases non-linearly when the duration of investment ( n ) increases.

Example of simple vs compound interest

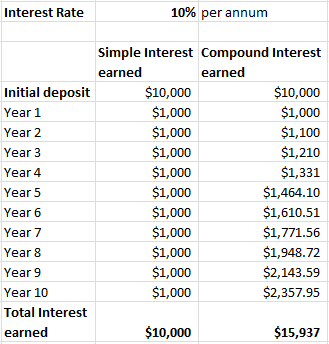

An example of the magic of compounding.

Let’s say you deposited $10,000 and saved it in the bank for 10 years and had an interest rate of 10%. If you earned 10% simple interest every year, you would finish the 10 years with a total interest income of $10,000 (I = 10,000 x 0.10 x 10).

However, if the interest was compounded, the interest income in each year would be higher than the previous year. And at the end of 10 years, you would have earned $15,937 in interest.

Why is interest charged?

Interest is not always charged when money is borrowed. For example, when borrowing from friends, parents or other relatives, the lender may choose to not demand interest. However, there are several reasons for interest to be justifiably charged, including:

- Risk of default : It is possible that the borrower may not repay the money. The risk of default is different for each borrower; more credit-worthy borrowers have a lower risk of default. Nevertheless, there is always a risk and the lender ought to be compensated for this risk.

- Opportunity cost : The lender could gainfully employ the capital elsewhere instead of lending to the borrower. This is called opportunity cost. By lending the money to a specific borrower, the lender closes all other avenues to use it for gain.

- Inflation : The value of money decreases with time because of inflation. If $100 is lent today and will be repaid 3 years from now, the same $100 will be worth equivalent to only $98 today.

The rate of interest depends upon all these factors but there are usually usury laws that prohibit charging interest above a certain rate. Throughout history there have been many laws and religious prohibitions on usury.

References

- wikipedia:Interest

- wikipedia:Compound interest